US Economic Outlook

Investors await the FED’s next rate announcement next week, making it the ideal time to discuss the US economic outlook.

There experts who don’t like the 6 month forecast believing the lagging effects of the high rates are now kicking in and will persist. Whether that weighs on the stock market or not remains to be seen. After all, if rates drop by 1% by year end, that could give both stocks and the economy a nice boost.

In this post on the 2025 economic outlook, several factors come into focus:

- the Presidential election will be the number one factor for the economic forecast and stock market forecast

- if Trump raises import tariffs, commits to US businesses, repatriates manufacturing, pivots on AI technology, grows energy supply, reduces regulations, and lowers taxes, it should give the US economy a significant boost

- xChina is becoming more real every day and US companies are leaving the communist country quietly returning home

- investors are bringing investment dollars back expecting the US to be the only place to invest in

- wars with Russia and China aggression will play havoc with supply chains

- oil prices and oil production will lower inflation initially then likely bring it back in 2025/2026

- lower interest rates will aid in growing US small business and easing stress on consumers

- inflation has been easing for some time now and core CPI hit 2.5% in August

- GDP growth is expected to slow this fall/winter and return above 2% in late 2025

- unemployment is up slightly but wage growth has been healthy

- AI technology is being kept under reign and away from enemies and those seeking unfair advantage (technology transfer)

- AI era will create product upgrades followed by a complete overhaul of software and systems in next ten years resulting in large investors feeling confident about going all in on that.

- a cultural shift toward conservative values and a rejection of further immigration should ease government spending

Of all factors, US manufacturing repatriation and business support combined with the AI revolution will likely be the foundation of the great US economic rebirth and continuous US GDP growth.

The elections are still a wild card, and the country could slip back into socialism or worse. There are huge threats. The budget deficit, national debt, interest payments on the national debt, and dependence on China that are vulnerabilities for enemies to exploit.

Powerful, Tech-Enabled, Resourceful Economy Looking to Grow

The US economy has huge potential and really, more stimulus is not needed. Investors have plenty of cash in money markets to move to equities including small businesses. With lower lending rates, and lower mortgage rates, small business owners will finally get relief in the years ahead as they attempt to restart and grow.

Inflation Has Fallen

Alan Blinder, a Princeton University economist said “The sooner the inflation rate falls, the sooner the Fed will ease up, and therefore the less the chance of a recession.”

He couldn’t foresee that Powell and company would push it to the edge, with FED brinksmanship. Infaltion has fallen without the FED offering much reward to US citizens and mortgage holders. Just persistent pain for Americans.

In a few days, we’ll know whether they’ll be greedy and keep it high or show they want the economy to recover. With a Trump victory, Powell and company may be seeing their last days in office. A new FED governor would look for a fresh new start for the FED and for the US economy.

CPI data by Truflation. Screenshot courtesy of Truflation.

Can an economy bursting with millennial/Gen Z demand, high immigration, cash rich consumers and ultrawealthy corporations be contained?

2025 is the Year of the Upward Launch

2025 could have been a revival year but the FED ensured it wasn’t. But without growth in supply, that early rebirth would have likely created strong inflation. Now with the economy cooling, we’re seeing oil prices drop, consumer prices flatten, and businesses refusing to build supplies.

As Trading Economics chart shows, manufacturing has been badly injured with a rapidly declining index due to high interest rates and business de-risking.

Further, Trading Economics sees US manufacturing enjoying a return for the next 3 years. The extent of that positive growth depends on many variables however, so it’s a shaky kind of forecast.

China Manufacturing and Investment Brought Back to America

The biggest single factor in a recovery is in onshoring investment/manufacturing that China has taken for the last 20 years.

This change in relations between the US and China, which I call xChina is quickening. The Democrats resisted the breakup but now with China dumping its excess production, the US is forced to counter with new tariffs on China imports. This is creating further political friction and brinksmanship could cause supply issues and market turmoil. Expect the Dow Jones to show volatility until the US gets on solid footing for its manufacturing. The US will look to Taiwan, Vietnam, India, Mexico and Canada for relief as the US-China breakup and competition roll out.

What are the Top Economic Indicators to Watch?

- GDP growth for Q4, 2024 and full year 2025

- consumer confidence

- FED lending rate

- unemployment and job creation

- industrial production

- consumer spending

- inflation rate

- housing market

- new homes sales

- retail spending and business spending

- cost of energy

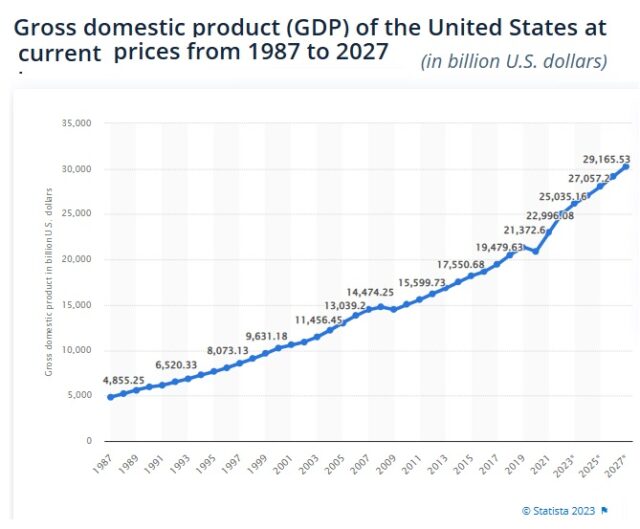

US GDP Rolls Along

The 5 year outlook for GDP remains solid despite previous warnings from economists a flat economy for the next decade. Where there’s money and spending, there is employment and GDP growth. Investment money will return to rebuild America.

Macro warnings: The end of US FED stimulus, a fast tightening M2 money supply, rising interest rates to fight high inflation, pandemic-weakened consumer demand and supply chains, along with being at the end of a long bull run, super high housing prices, and the debt limit crisis were macroeconomic warnings that until recently held weight.

Yet at this point, we can see the light at the end of the FED tunnel.

About Supply and Inflation

One point of contention is about supply to markets. Supply chains did finally become unblocked however regulations continue to suppress American freedom and productivity. This all based on ideological concepts with no regard to the political and economic long term consequences.

Oil, housing, copper, and other commodities are over-regulated, thus artificially suppressing supply and raising prices. For example, raising the lending rate is forcing the cost of home ownership up, thus fueling more inflation — the kind that risks a housing market crash. We’re not through that worry yet.

The FED is focusing on controlling demand for cars, furniture, credit, fuel, and discretionary goods. Yet demand for heating fuel, electricity, gasoline, food, and other staples are difficult to suppress. Rent prices too in a market without vacancies is impossible to suppress. 12-month leases are signed, and even after expiring, renters have little room for negotiation with landlords. With nowhere to go, renters must pay up.

Without a massive construction effort, housing is going to suffer for some time. Rents have only fallen minimally, and in some cities are up strongly in the last year (34% in some cities). And with workers demanded to be back in office in crowded urban head offices, some cities won’t see a rent reprieve.

A New President in 2024: A New Life for the American People

A new US President in 2024, and balance of power changes in the US Senate and house of representatives could result in a full scale revival of US oil production, thus pushing oil prices well down. Cheap energy drives cheap business from microchips to transportation. Add on AI reconstruction of the economy, and how could it not boom?

Expect more volatility in the 2023/2024 markets. See more about the S&P, Dow Jones, and NASDAQ.

* the above post includes opinions of the author and do not connote recommendations of any kind regarding stocks to invest in. The material is provided as general information only. For all your stock investment decisions please refer to your financial investment advisor.