US Real Estate & Housing Market Predictions

The US housing market forecast has a wide variety of information and views depending on the interest of readers such as buyers, sellers, Realtors, mortgage agents, home flippers, builders, politicians, and more.

Although the newly elected Trump government is a boost for the US economic outlook, its first year will likely continue to be volatile with setbacks and surges as repatriation of business, manufacturing and employment to America grows.

The economy however seems uncertain, and the growing issue with an international trade war and the destruction of the USMCA trade agreement, are making buyers hold off on putting offers in for homes. However, it is giving the green light to home sellers to unload before a potential recession or a price decline. But that decline doesn’t look too likely.

Key Factors Affecting Price Predictions

The key to the housing market forecast and quality predictions revolves around affordability and the US economic outlook. Although the economy is surging, Americans can’t qualify for the homes available. The level of income required to qualify for high rate (7%) mortgages, and the lack of affordably-priced homes available is reducing sales (which dropped almost 5%).

Statistics are skewed by the sales of upper-priced homes above $750,000. Without them, the picture looks much dimmer.

Realtor.com® Chief Economist Danielle Hale says: “If people feel like the market itself is not able to meet their needs, then it’s not surprising to see them look to politics to try to find a solution.”

Politics and macroeconomics are once again pivotal in any homebuying decision. While President Trump is creating great friction and waves politically, his actions are seen as noisy negotiating positioning to help the US get a better deal, and to grow the US economy. Out of all, he is clearly insistent on the US getting a fair deal in trade, and is asserting himself. In the face of a global trade war, countries trading with the US will be forced to lower their tariff walls or suffer economically.

How Do US Realtors Feel about the Housing Market?

Real estate agents across the country are intimately tuned to the state of the market. Their feelings and perspective are vital information for you as a buyer or seller. Realtors appear less optimistic about the market, see homes sitting longer, and fewer homes selling above list price. Work from home and virtual buying are a demand trend for Realtors to explore.

Resistance to Trump’s negotiating tactics are growing, but it could lead to a global recession, and not hamper the US itself, which can live off of its own domestic productivity. Yet, supply is needed, and this is where inflation could rise significantly until all nations agree to play fair. Lumber, energy, electricity, copper, and more are needed if housing is to be affordable.

It is not inconceivable that a housing market crash event could occur. An economic calamity could send financial shockwaves into the housing market, ending new construction, and setting off a wave of foreclosures and selloff. Those refinancing at much higher lending rates are still in a precarious situation financially.

According to Census.org, new housing starts and permits are lagging as we head into the new year. They report that privately-owned housing starts in January fell 9.8% in January vs December. Single-family housing starts in January fell 8.45 vs December.

The National Association of Realtor’s most recent report shows home supply (+3.0%), sales (-4.8%) and home prices (+4.9%) are increasing. Affordability improved only slightly and due to slightly lower mortgage rates and payments. The median annual qualifying income to buy a home fell slightly to $102,480.

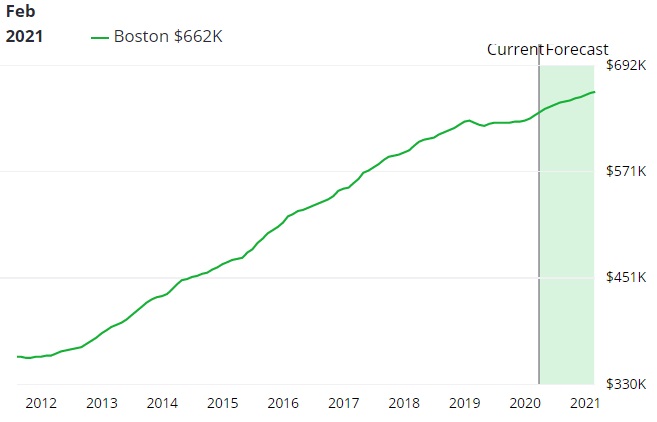

As you can see in this chart below, home prices are risi ng on a long term trend and there is little to believe this won’t continue. With a fast growing economy, even with higher inflation, the price trend is likely to grow. More jobs, higher incomes, and a strong demand for housing can only mean higher prices. Even with a temporary Trumpcession, demand is simply too strong, especially in the affordable housing category.

Corelogic believes home prices will rise 3.6% over the next year.

Housing Market Activity in January

Did January’s home sales seem to agree with the longer term trends?

NAR reports that:

- Existing home sales decreased 4.9% in January to a seasonally adjusted annual rate of 4.08 million. Yet, year over year, home sales did grow 2.0% which is the fourth straight monthly year-over-year increase.

- The median existing home price rose 4.8% from January 2024 to $396,900, and that is the 19th consecutive month of year-over-year home price increases.

- Existing home supply rose 3.5% from the prior month to 1.18 million at the end of January, or the equivalent of 3.5 months’ supply at the current monthly sales pace.

Given the high average prices across US states and cities, combined with still high mortgage rates in the 7% range, few buyers can afford to purchase a home. With wealthy parents pulling back on financing a home for their 20 to 35 year old children. First time buyers decreased 3% to 28% of the sales market.

“Mortgage rates have refused to budge for several months despite multiple rounds of short-term interest rate cuts by the Federal Reserve,” said NAR Chief Economist Lawrence Yun. “When combined with elevated home prices, housing affordability remains a major challenge.”

Freddie Mac, reports the 30-year fixed-rate mortgage averaged 6.85% as of February 20th, 2025, a .03% drop from 6.87% one week ago and down .06% from 6.90% last February. With a strong jobs report this week, there’s little reason to believe inflation won’t be an issue this year. Thus we might forecast interest rates to rise, and for long term bond prices to rise with the view of longer term inflation outlooks. It will be tough for mortgage rates to decline anytime soon.

Sales of single-family houses fell 5.2% to a seasonally adjusted annual rate of 3.68 million in January, yet that is still 2.2% higher than last January 2024. The median existing single-family house price rose 5.0% to $402,000 in January, up 5.0% vs 12 months ago.

Existing condo and co-op sales slid 2.4% in January to a seasonally adjusted annual rate of 400,000 units, same as last year. The median existing sold condo price rose 2% to $349,500 in January, and that was 2.9% from January 2024 ($339,500).

All regions in the US are not the same. Home sales and prices vary from east to west.

- In the Northeastern region, existing-home sales fell 5.7% from December to an annual rate of 500,000, up 4.2% from January 2024. The median house price in the Northeast was $475,400, up 9.5% from one year earlier.

- In the Midwest, existing-home sales remained the same year over year. Sales stayed at an annual rate of 1 million, (+ 5.3% vs 12 months ago). The median home price in the Midwest rose a strong 7.2% to reach $290,400.

- In the Southern region, existing-home plunged 6.2% vs the previous month, to an annual rate of 1.83 million in January. The median home price however, still rose 3.5% year over year to reach $356,300.

- In the West, existing-home sales slumped 7.4% in January vs December 2024 to an annual rate of 750,000. That is still up 1.4% from a year ago. The new median price in the West rose a strong 7.4% vs 12 months ago to reach $614,200.

Homes sales in the affordable range, across the country fell 14.2% while homes above $1 million have surged an average of 26.9% with sales growing 51% in the Northeastern region.

Issue: Supply of Homes for Sale

Reasons Why People Are Still Eager to Buy Real Estate:

- home prices are appreciating and it’s a safe investment over the long term

- millennials desperately need a home (house/townhouse) to raise their families

- rents are high giving property owners excellent ROI on rental properties owned

- flips of fixer-uppers and older properties continue to create amazing returns

- real property is less risky (unless you get over-leveraged)

- the economy will improve by late 2024

- a homebuying frenzy is ahead by 2025 as economy is unleashed (election hopes!)

Will 2025 Be Better?

- there will be more homes listed

- prices may pick up pace (depending on political outcome)

- the economy will regrow (the pro-USA movement is a strong indicator)

- new construction will continue

- mortgage rates will remain elevated and credit hard to get

- competition for homes will ease off

- some sellers will find it easier to sell and move on with their lives as rates fall

- home price growth will moderate a little (estimates down to 2% growth by NAR, 4.8% by MBA, and 5.9% by Zillow)

US Home Sales Forecast to 2026

Below, Statista’s research team believe home sales will rise only slightly in the coming 2 year time period.

Zillow’s Home Price Predictions

Zillow’s home price forecast were very optimistic but of late they’ve moderated their projections.

Zillow forecasts home values to rise 0.9% this year (down 2.9% from previous prediction). New listings were higher than expected out of the gate this year. House inventory expectations that were revised higher have put downward pressure on Zillow’s forecast for home prices.

Call Gord about Realtor marketing Services.