Bitfarms Ltd. (NASDAQ: BITF): A Vertical Shift Upward to AI Infrastructure

Bitfarms, founded in 2017 and headquartered in Toronto, Canada, initially established itself as a global, vertically integrated Bitcoin mining company. Its stock price is on a bit of a tear of late, and you might be wondering if there is still an opportunity in the (Nasdaq: BITF) stock which is also listed on the Toronto TSX in Canadian currency.

Bitfarms’ shares have rocketed 400% in the last six months and are up +194.6% for 2025. Its crash as seen in the Google Finance graph was due to the Bitcoin halving event which reduced their profit margins, yet the company adapted to instead focus to high-performance computing (HPC) and artificial intelligence (AI) data centers, which are expanding rapidly and have the potential to generate higher profits than BTC mining. The future outlook is brighter here.

Bitfarms’ shares have rocketed 400% in the last six months and are up +194.6% for 2025. Its crash as seen in the Google Finance graph was due to the Bitcoin halving event which reduced their profit margins, yet the company adapted to instead focus to high-performance computing (HPC) and artificial intelligence (AI) data centers, which are expanding rapidly and have the potential to generate higher profits than BTC mining. The future outlook is brighter here.

What is Bitfarms?

Companies like Bitfarms (competitors named below) are quickly described to investors as global, vertically integrated digital infrastructure companies that build and manage data center infrastructure for Bitcoin mining and High-Performance Computing (HPC)/Artificial Intelligence (AI).

Bitfarms Ltd. (NASDAQ: BITF) is a global, vertically integrated digital infrastructure company that leverages its large-scale power access and data center footprint to generate revenue from two distinct sectors: Bitcoin Mining and High-Performance Computing (HPC)/Artificial Intelligence (AI) data center hosting.

A Successful Transition to Changing Cryptocurrency/Blockchain Opportunities

The industry trend of Bitcoin miners such as Bitfarms transitioning to AI is often referred to as the “Mullet Strategy“: AI data centers in the front, and Bitcoin mining in the back. Tech and AI Investors view these hybrid companies favorably (“hybrid miners”) as they offer a diversified revenue model compared to “pure play” Bitcoin miners.

The company’s core business involved designing, owning, and operating data centers across North America (Canada and the United States) and South America (Paraguay and Argentina) to validate transactions on the Bitcoin blockchain in exchange for cryptocurrency rewards.

The advantage of cheap electric power: Their original strategy was the opportunity of sustainable and low-cost energy. The company heavily utilized predominantly environmentally friendly hydro-electric power and long-term power contracts, giving it a competitive edge in electricity costs, which are the single largest operational expense in crypto mining.

Here, Yahoo Finance data shows a promising outlook for the company’s revenues:

| Currency in USD | Current Qtr. (Sep 2025) | Next Qtr. (Dec 2025) | Current Full Year (2025) | Next Full Year (2026) |

| No. of Analysts | 8 | 8 | 8 | 7 |

| Avg. Estimate | $85.73M | $86.84M | $317.06M | $330.71M |

| Low Estimate | 77.14M | 69.32M | 293.23M | 248.13M |

| High Estimate | 95.24M | 100.9M | 337.2M | 448.4M |

| Year Ago Sales | 44.85M | 56.16M | 192.88M | 317.06M |

| Sales Growth (year/est) | 91.13% | 54.62% | 64.38% | 4.30% |

The Strategic Shift: From Bitcoin Mining to AI/HPC

The most recent Bitcoin halving event and the surging, high-margin demand for AI infrastructure have spurred a crucial and accelerating strategic pivot for Bitfarms. While Bitcoin mining remains a stable, low-capex business providing a cash flow foundation, the future growth is firmly focused on High-Performance Computing (HPC) and Artificial Intelligence (AI) data centers. Bitfarms is viewed as one of the leaders in this area.

However, a major part of Bitfarms’ revenue comes directly from mining Bitcoin, and BTC’s price forecasts are rolling upward dragging Bitfarms stock price up with it.

Just as competitors IREN and Hut 8 have successfully done, the company is repositioning its extensive energy portfolio and modular data center infrastructure to service the high-density computing needs of AI and HPC clients. This shift is designed to unlock higher-margin, more predictable, and long-term revenue streams compared to the volatile nature of cryptocurrency mining. The strategy involves:

- Repurposing Data Centers: Modifying existing and development-stage data center facilities to be capable of hosting power-intensive AI hardware, such as advanced GPUs.

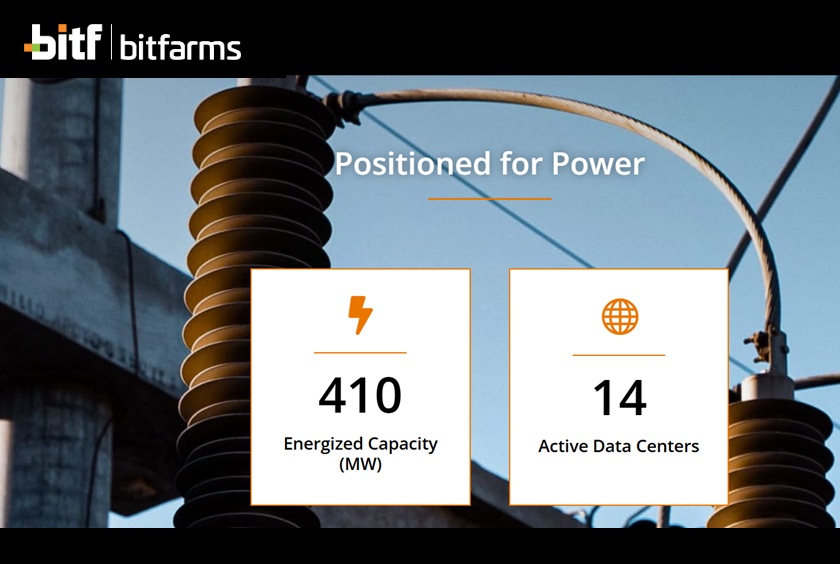

- Focusing on North America: Significant expansion efforts are concentrated in the U.S., particularly with the acquisition of power campuses in Pennsylvania (e.g., the flagship Panther Creek campus) and other data center hotspots like Washington and Quebec, leveraging its total energy pipeline of approximately 1.4 GW, over 80% of which is U.S.-based.

- Vertically Integrated Advantage: Continuing to utilize its vertically integrated model—which includes in-house electrical engineering and management—to optimize the design and operation of these next-generation AI data centers.

What is the Demand for Bitfarms’ Services

The demand for Bitfarms’ evolving services is split across its two primary business segments:

- Bitcoin Mining (Foundational Revenue)

-

- Demand Source: The fundamental need for computational power (hashrate) to secure and process transactions on the Bitcoin network.

- The Cost/Reliability Niche: Bitfarms’ niche here is its low-cost, predominantly clean energy profile. This allows it to mine Bitcoin profitably even during periods of lower Bitcoin prices or after a halving event reduces mining rewards. Their high operational efficiency and low power costs bolster margins compared to competitors’ reliance on more expensive or less sustainable power sources.

- High-Performance Computing (HPC) and AI Data Centers (Growth Vector)

-

- Demand Source: This is the hyper-growth area driven by the “AI Industrial Revolution.” The insatiable demand for training and running complex AI models (like large language models), machine learning, and advanced scientific computation requires an unprecedented amount of high-density computing power and specialized data center capacity.

- The Niche: Bitfarms’ opportunity lies in its existing, large-scale, pre-wired energy infrastructure. Building new data centers is slow and capital-intensive. Bitfarms can convert its energy-rich sites, which are already connected to the grid and often utilize low-cost power, faster than new entrants can build from scratch. The company’s large energy pipeline in strategic US data center hubs is particularly attractive to prospective AI clients and partners looking for rapid, scalable deployment of GPU clusters.

The recent closing of a substantial convertible senior note offering (upsized to US$588 million) and a private debt facility (up to $300 million with a division of Macquarie Group for the Panther Creek project) validates the market’s belief in the commercial attractiveness of Bitfarms’ AI data center potential and its ability to attract significant institutional infrastructure financing.

Main Competitors of Bitfarms

Bitfarms operates in two highly competitive markets: the established Bitcoin mining sector and the emerging AI infrastructure hosting space.

Bitfarms Primary Competitors (AI & Bitcoin Mining):

The closest competitors are companies that have also been in the financial news. They are large-scale, publicly traded Bitcoin miners who are also pivoting into AI/HPC to diversify revenue and capitalize on their power assets.

- Riot Platforms, Inc. (NASDAQ: RIOT): One of the largest US-based Bitcoin miners with massive power capacity. Riot has been aggressive in its expansion and has also shown interest in capturing HPC/AI hosting revenue, often seen as a direct rival for power assets and industry leadership.

- Marathon Digital Holdings, Inc. (NASDAQ: MARA): Another major player with a focus on scale and strategic partnerships. Marathon is diversifying beyond mining into data center services and AI capabilities through strategic deals and investments, directly competing for AI hosting customers.

- Hut 8 Corp. (NASDAQ: HUT): Hut 8 has been one of the clearest “miner to AI host” transition stories, actively pursuing high-performance compute contracts and leveraging its diversified operations and managed infrastructure business.

- CleanSpark Inc. (NASDAQ: CLSK) and Cipher Mining Inc. (NASDAQ: CIFR): These and other large miners are primary competitors in the Bitcoin mining efficiency and capacity race, where they vie for the lowest cost of production and largest share of the global hashrate.

Secondary Competitors (Dedicated AI/HPC):

As Bitfarms pivots, it increasingly competes with dedicated high-performance computing and data center operators.

- CoreWeave (Private): A high-profile, fast-growing specialized cloud provider for AI, which has recently partnered with major tech players to secure significant energy and data center capacity.

- Traditional Data Center Providers (e.g., Equinix, Digital Realty): While often serving broader enterprise needs, their high-density compute offerings and new builds are directly competing for the same major AI customers.

Future Forecasts and Buy Ratings for BITF

The future outlook for Bitfarms is tied directly to the success of its strategic shift from a pure-play Bitcoin miner to a diversified energy and compute infrastructure company.

Analyst Consensus and Ratings

As of the latest available data, Wall Street analysts maintain a generally optimistic outlook, primarily driven by the high-margin potential of the AI pivot.

- Consensus Rating: The general consensus among analysts covering the stock often leans towards a “Strong Buy” or “Buy” rating, though this is caveated by high volatility and execution risk. For example, some analyst aggregates show 100% of tracked analysts recommending a Strong Buy or an equivalent “Outperform” rating.

- Price Targets: Analyst one-year price targets vary widely, reflecting the inherent volatility of both the crypto and emerging AI infrastructure markets. Recent price targets show a range, with the average one-year target hovering in the mid-range of its recent trading price, but specific bullish calls often project a significant increase from the current price, particularly those focused on the long-term AI upside.

Future Financial Forecasts

Financial forecasts highlight the expected benefits of the AI pivot:

- Revenue Growth: Analysts project very strong revenue growth over the next few years. For instance, revenue is forecast to grow by a high double-digit percentage annually (e.g., over 35-50% per year) in the near to medium term, driven by new AI/HPC contracts coming online at the newly developed U.S. sites.

- Profitability: Bitfarms has historically been unprofitable on a GAAP basis. The shift is intended to reverse this, with positive earnings per share (EPS) often projected within the next two years. The higher margins associated with HPC/AI contracts are expected to significantly improve Gross Profit and Adjusted EBITDA.

Key Risks and Considerations for BITF Investors

Despite the bullish sentiment surrounding the AI pivot and recent capital raise, significant risks remain:

- Execution Risk: The successful transition to a premium AI data center operator requires complex buildouts, securing long-term HPC contracts, and successfully integrating new assets. Any regulatory delays in converting mining capacity or construction delays could stall the transition.

- Bitcoin Volatility: While diversifying, Bitfarms remains materially exposed to the price of Bitcoin, as mining still constitutes the bulk of its current revenue. Bitcoin price drops could negatively impact cash flow and stock performance.

- Profitability: The company is currently unprofitable, and the net profit margin is still significantly negative, lagging behind some industry peers. Sustained execution is needed to close this gap.

- Dilution: The recent upsizing of its convertible notes offering, while providing vital capital, also introduces the risk of shareholder dilution upon conversion.

Is Bitfarms a Good Stock to Buy?

Bitfarms Ltd. (BITF) represents a speculative but potentially profitable investment capitalizing on low-cost energy for data centers, digital infrastructure, and the explosive demand for AI computing power.

Bitfarm’s established, vertically integrated, and cost-efficient Bitcoin mining operation provides a stable base of revenue. Yet, the true investment narrative is its successful and accelerating strategic pivot to AI/HPC data center hosting, backed by substantial recent financing (over $1 billion in cash, Bitcoin, and available funds). This pivot leverages its large, underutilized power assets in key North American regions to chase high-margin, predictable revenue.

For risk-tolerant investors, Bitfarms is positioned to be a key beneficiary of the AI data center boom, using its unique access to low-cost power as a significant competitive moat. The strong consensus from analysts to a “Strong Buy” or “Outperform” rating reflects the excitement around this transformative strategy, but investors must weigh this against the inherent risks of execution, regulatory hurdles, and persistent crypto-market volatility.

The Barchart Technical Opinion rating shows a 96% Buy with a Strongest short-term outlook on maintaining the current direction.

See more on the macroeconomic view of the US stock market before researching the best stocks to buy including the best AI stocks to buy. Is the AI stock bubble about to burst and should you buy rare earth stocks?

* Disclaimer, The information collected and synthesized in this report was conducted in part via AI search engines. Please review and verify all statements, info and buy ratings related to any stocks you’re researching online. AI is playing a significant role in all financial media now, and can make key errors. See more on effective SEO/GEO content optimization techniques.